Overpay Your Mortgage or Invest? What the Numbers Say

i4sys:mortgage-overpay-001

Overpay Your Mortgage or Invest? What the Numbers Say Right Now

If you find yourself with spare cash each month, the pressing question is whether to overpay your mortgage or invest that money instead. This decision has become increasingly critical as mortgage rates have surged, impacting many homeowners across the UK.

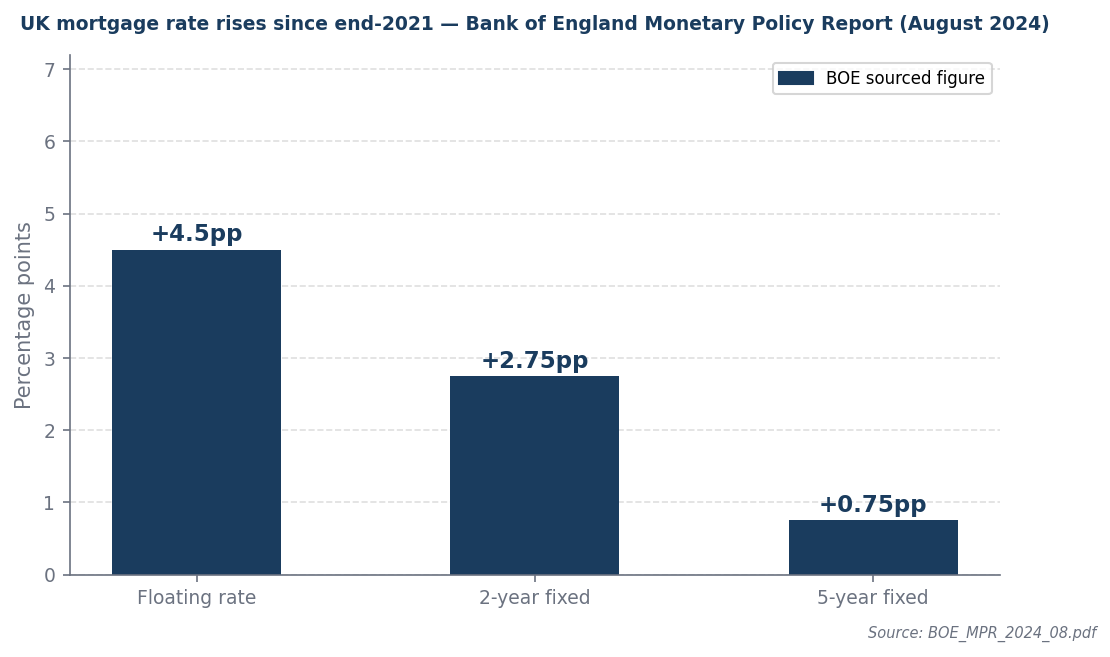

With the Bank of England reporting a significant rise in mortgage costs, especially for those transitioning from fixed-rate deals, the stakes are higher than ever. As of August 2024, the average rate on outstanding UK floating rate mortgages has increased by 4.5 percentage points since the end of 2021, making the choice between overpaying and investing a pivotal one for many households.

The real decision

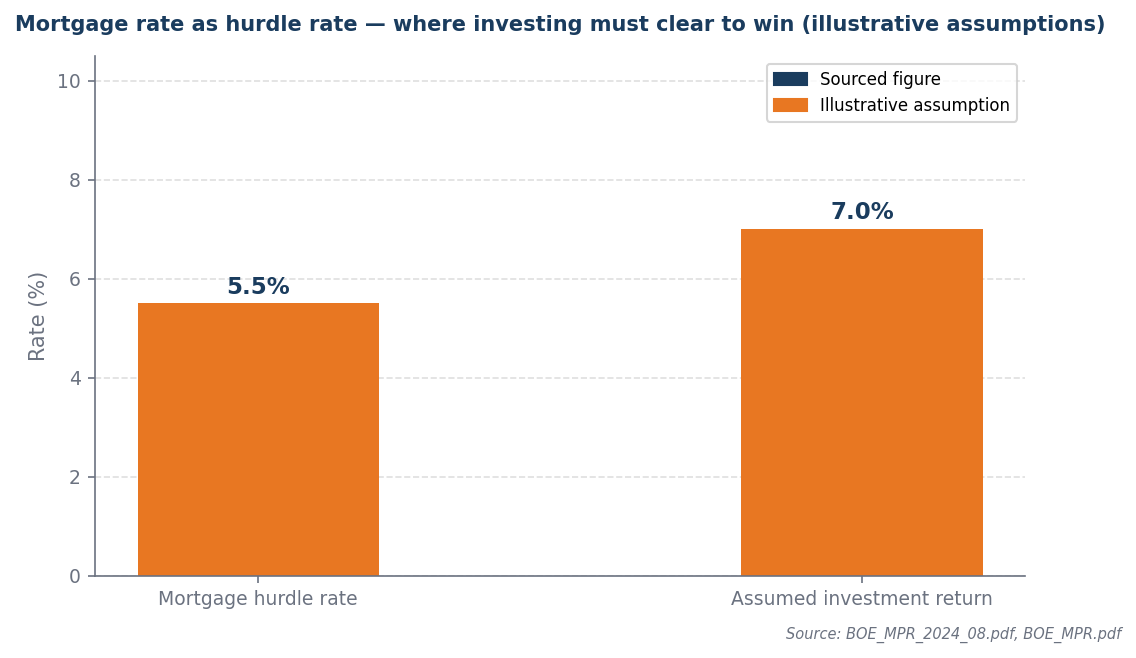

Overpaying your mortgage effectively gives you a return equal to your mortgage rate, which acts as your hurdle rate. For instance, if your mortgage rate is 5.5%, every pound you overpay saves you 5.5% in interest before tax. This is a compelling return that is difficult to match with investments, especially in a volatile market.

As many homeowners are facing payment shocks, with nearly half of all mortgages expected to see payment increases between December 2024 and early 2028, the decision becomes even more pressing. The Bank of England's Monetary Policy Report highlights that a significant portion of borrowers will soon experience higher monthly payments, making overpayment a potentially wise strategy to mitigate future financial strain.

When overpaying wins

Overpaying your mortgage tends to be the better option when your current mortgage rate is high, particularly if you are nearing the end of a fixed deal. With many borrowers facing increased payments, the immediate savings from overpaying can provide much-needed relief in cash flow.

Additionally, if your household budget is likely to tighten due to rising mortgage costs, overpaying can help reduce the overall debt burden. This strategy not only lowers your monthly outgoings in the future but also provides a clear path to financial stability amidst rising interest rates.

Worked example

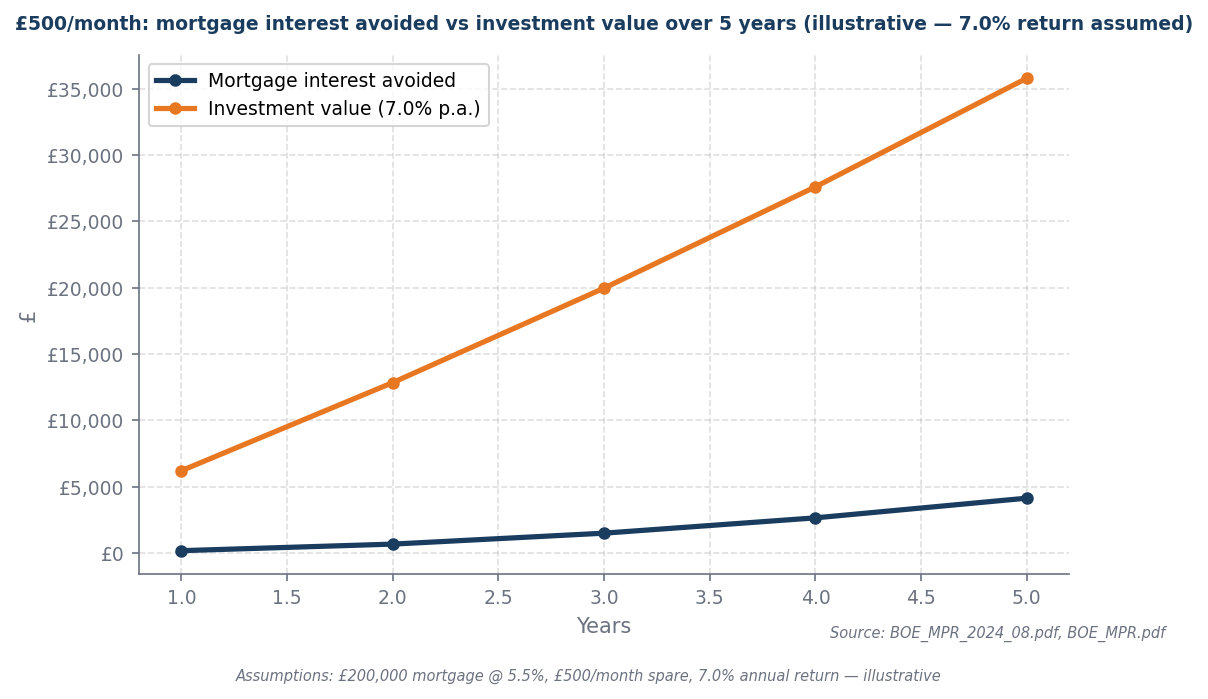

Consider a borrower with a mortgage balance of £200,000 at a current mortgage rate of 5.5% (illustrative assumption). If they have £500 in spare cash each month (illustrative assumption), they face a choice: overpay their mortgage or invest that money. Over the next five years, the mortgage interest avoided by overpaying would be as follows: Year 1: £165, Year 2: £660, Year 3: £1,485, Year 4: £2,640, Year 5: £4,125 (illustrative assumption).

In contrast, if the same borrower invests the £500 monthly at an assumed return of 7.0% per annum (illustrative assumption), the investment value would grow significantly over the same period: Year 1: £6,196, Year 2: £12,841, Year 3: £19,965, Year 4: £27,605, Year 5: £35,796 (illustrative assumption). This stark contrast highlights the potential benefits of both strategies.

Ultimately, the decision hinges on whether the immediate savings from overpaying outweigh the potential long-term gains from investing. With rising mortgage costs, many may find that overpaying offers a more secure and visible return in the short term.

When investing wins

Investing can still be the superior choice under certain conditions. If your mortgage rate is relatively low, and you have a long investment horizon, the potential for higher returns from investments may outweigh the benefits of overpaying your mortgage. For example, if your mortgage rate is below 3%, investing could yield greater wealth accumulation over time.

Moreover, if you have already established a solid emergency fund, investing spare cash can provide opportunities for growth that may not be available through mortgage overpayment. The key is to balance the potential for returns against the certainty of savings from overpaying.

Mixed strategy

- Clear expensive debt first. Prioritise paying off high-interest debts like credit cards before considering mortgage overpayment or investing.

- Protect cash reserves. Ensure you have sufficient savings set aside for emergencies before committing to either strategy.

- Use overpayments to reduce rate pressure. This can help improve your financial resilience if your mortgage rate increases significantly.

- Invest what remains if your horizon is long enough. This allows you to take advantage of market growth without compromising your immediate financial stability.

This mixed strategy allows for flexibility in managing your finances while maximising potential returns and minimising risks associated with rising mortgage costs.

Bottom line

In the current climate, where mortgage rates are high and rising, overpaying your mortgage often emerges as the more practical choice. The immediate savings are tangible and provide a clear benefit in a time of financial uncertainty.

Investing may offer long-term gains, but with the current landscape, the mistake is to overlook the immediate advantages of reducing your mortgage burden. Run the numbers carefully and consider your personal circumstances before making a decision.