Overpay Your Mortgage or Invest? The Numbers Say

i4sys:mortgage-overpay-001

For most UK borrowers at 5.5%, overpaying your mortgage is the stronger move right now.Confidence: mediumThis verdict holds while your mortgage rate remains above the expected return assumption and your investment horizon does not materially exceed 5 years.

The rate decision

Overpaying only loses if after-tax returns clear the mortgage hurdle by enough to justify volatility.

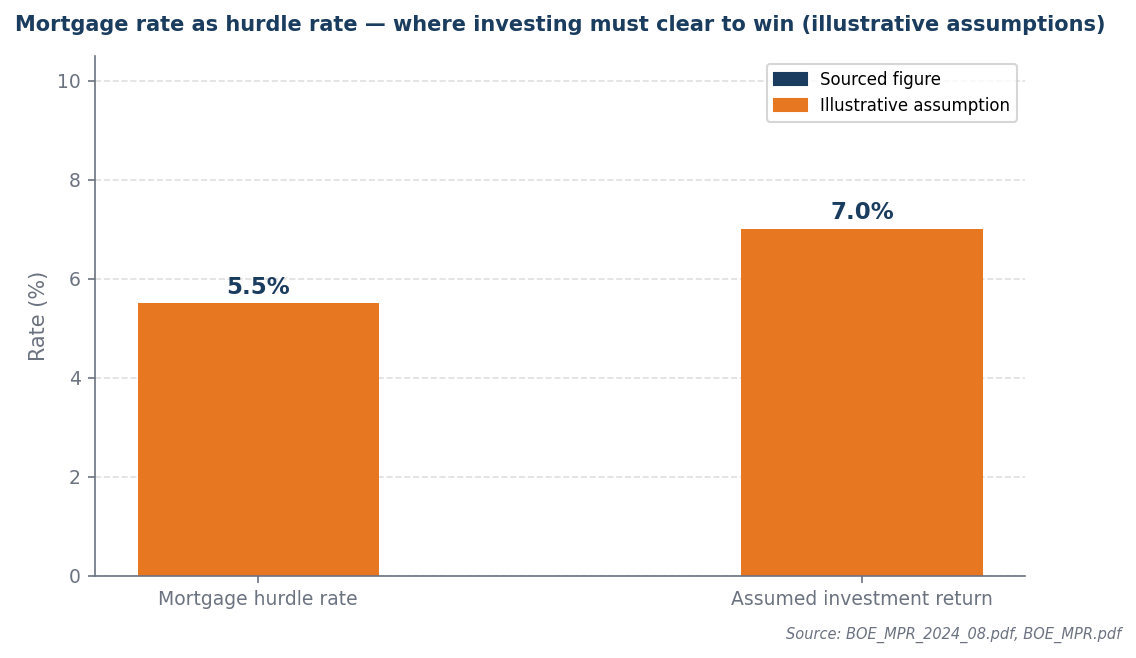

A mortgage rate of 5.5% serves as a critical hurdle rate because it establishes the minimum return required to justify the risk of investment. With an expected return of only 7.0%, the 1.5 percentage point spread is insufficient to compensate for the inherent volatility and uncertainty associated with market investments. This narrow margin fails to provide a robust buffer against potential downturns, making it a poor choice for risk-averse investors. Therefore, the investment does not clear the hurdle rate with adequate confidence, warranting a reevaluation of the risk-return profile.

The rate backdrop

Rate rises since 2021 mean the case for overpaying is materially stronger than it was when mortgage costs were ultra-low.

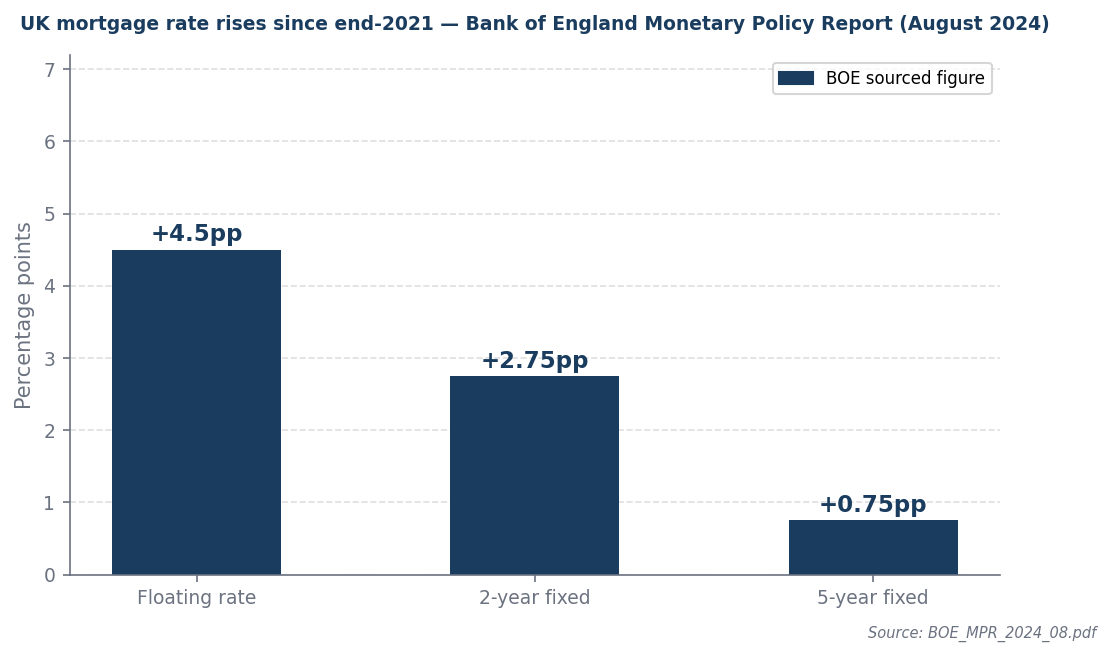

Since 2021, the Bank of England's rate rises have significantly impacted UK mortgage borrowers, with floating rates increasing by 4.5 percentage points and 2-year fixed rates climbing by 2.75 percentage points, while 5-year fixed rates have risen by 0.75 percentage points. This environment of higher borrowing costs makes overpaying on mortgages more compelling, as borrowers can reduce their principal faster and minimize interest payments over time, especially given the potential for further rate increases. Additionally, with fixed rates still elevated, locking in lower monthly payments through overpayments can provide substantial long-term savings and financial stability. Consequently, the current backdrop strongly favors proactive debt management strategies like overpaying to mitigate the impact of ongoing rate volatility.

Worked example

£200,000 mortgage5.5% mortgage rate£500/month spare7.0% assumed investment returnAll figures illustrative

| Year | Mortgage interest avoided (certain) | Investment profit above contributions (illustrative) | Who is ahead |

|---|---|---|---|

| Year 1 | £165 | £196 | invest profit ahead by £31 |

| Year 2 | £660 | £841 | invest profit ahead by £181 |

| Year 3 | £1,485 | £1,965 | invest profit ahead by £480 |

| Year 4 | £2,640 | £3,605 | invest profit ahead by £965 |

| Year 5 | £4,125 | £5,796 | invest profit ahead by £1,671 |

By year 5, investment profit (£5,796) exceeds the overpayment saving (£4,125) by £1,671 — but only if the 7.0% return assumption holds without major drawdowns.This comparison flips if the investment return assumption falls below 5.5% or the mortgage rate rises materially. It also flips if the investment horizon shortens below 5 years.

When this flips

This flips only when the investment return exceeds the mortgage rate by more than 2.0 percentage points with high confidence, and the borrower has a long enough horizon to absorb volatility. In this scenario, the investor can leverage the lower cost of borrowing to amplify their returns through investments that yield significantly higher returns than the cost of the mortgage. A long investment horizon allows the investor to ride out market fluctuations, ensuring that short-term volatility does not derail their financial strategy.

For this condition to hold true, the mortgage rate must be stable and low, ideally below 4%, while the investment return must consistently exceed 6% over the long term. Additionally, the investor should have a minimum investment horizon of at least 10 years to effectively mitigate risks associated with market downturns. This combination of favorable rates, robust returns, and a sufficient time frame creates a compelling case for prioritizing investment over mortgage repayment.

What to do next

Rate above expected returnOverpay firstThe saving is immediate and certainLow rate with long horizonInvest firstThe hurdle is low enough to clear with timeUncertain incomePreserve liquidityNeither path works without a cash bufferMixed caseSplit strategyReduces fragility while capturing some upside

Sources and provenance

- Bank of England Monetary Policy Report (August 2024)

- BOE_MPR.pdf

- Bank of England Monetary Policy Report (November 2024)

Data as of: 2026-03-20